2018 Federal Budget Highlights for Business

The government’s 2018 federal budget focuses on a number of tax tightening measures for business owners. It introduces a new regime for holding passive investments inside a Canadian Controlled Private Corporation (CCPC). (Previously proposed in July 2017.)

Here are the highlights:

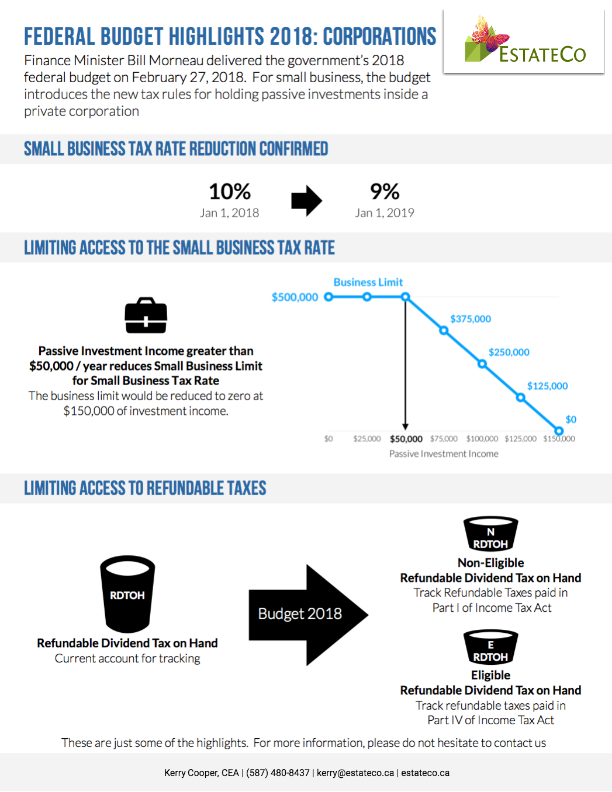

Small Business Tax Rate Reduction Confirmed

Lower small business tax rate from 10% (from 10.5%), effective January 1, 2018 and to 9% effective January 1, 2019.

Limiting Access to the Small Business Tax Rate

A key objective of the budget is to decrease the small business limit for CCPCs with a set threshold of income generated from passive investments. This will apply to CCPCs with between $50,000 and $150,000 of investment income. It reduces the small business deduction by $5 for each $1 of investment income which falls over the threshold of $50,000. This new regulation will go hand in hand with the current business limit reduction for taxable capital.

Limiting access to refundable taxes

Another important feature of the budget is to reduce the tax advantages that CCPCs can gain to access refundable taxes on the distribution of dividends. Currently, a corporation can receive a refundable dividend tax on hand (known as a RDTOH) when they pay a particular dividend, whereas the new proposals aim to permit such a refund only where a private corporation pays non-eligible dividends, though exceptions apply regarding RDTOH deriving from eligible portfolio dividends.

The new RDTOH account referred to “eligible RDTOH” will be tracked under Part IV of the Income Tax Act while the current RDTOH account will be redefined as “non-eligible RDTOH” and will be tracked under Part I of the Income Tax Act. This means when a corporation pays non-eligible dividends, it’s required to obtain a refund from its non-eligible RDTOH account before it obtains a refund from its eligible RDTOH account.

Health and welfare trusts

The budget states that it will end the Health and Welfare Trust tax regime and transition it to Employee Life and Health Trusts. The current tax position of Health and Welfare Trusts are linked to the administrative rules as stated by the CRA, but the income Tax Act includes specific rules relating to the Employee Life and Heath Trusts which are similar. The budget will simplify this arrangement to have one set of rules across both arrangements.